Global airline Delta Air Lines (NYSE:DAL) reported Q3 CY2025 results exceeding the market’s revenue expectations, with sales up 6.4% year on year to $16.67 billion. Guidance for next quarter’s revenue was optimistic at $16.03 billion at the midpoint, 2.2% above analysts’ estimates. Its GAAP profit of $2.17 per share was 39.8% above analysts’ consensus estimates.

Is now the time to buy Delta? Find out by accessing our full research report, it’s free for active Edge members.

Delta (DAL) Q3 CY2025 Highlights:

- Revenue: $16.67 billion vs analyst estimates of $16.06 billion (6.4% year-on-year growth, 3.8% beat)

- EPS (GAAP): $2.17 vs analyst estimates of $1.55 (39.8% beat)

- Adjusted EBITDA: $2.3 billion vs analyst estimates of $2.23 billion (13.8% margin, 3.2% beat)

- Revenue Guidance for Q4 CY2025 is $16.03 billion at the midpoint, above analyst estimates of $15.68 billion

- EPS (GAAP) guidance for the full year is $6 at the midpoint, missing analyst estimates by 10.8%

- Operating Margin: 10.1%, up from 8.9% in the same quarter last year

- Free Cash Flow was $687 million, up from -$54 million in the same quarter last year

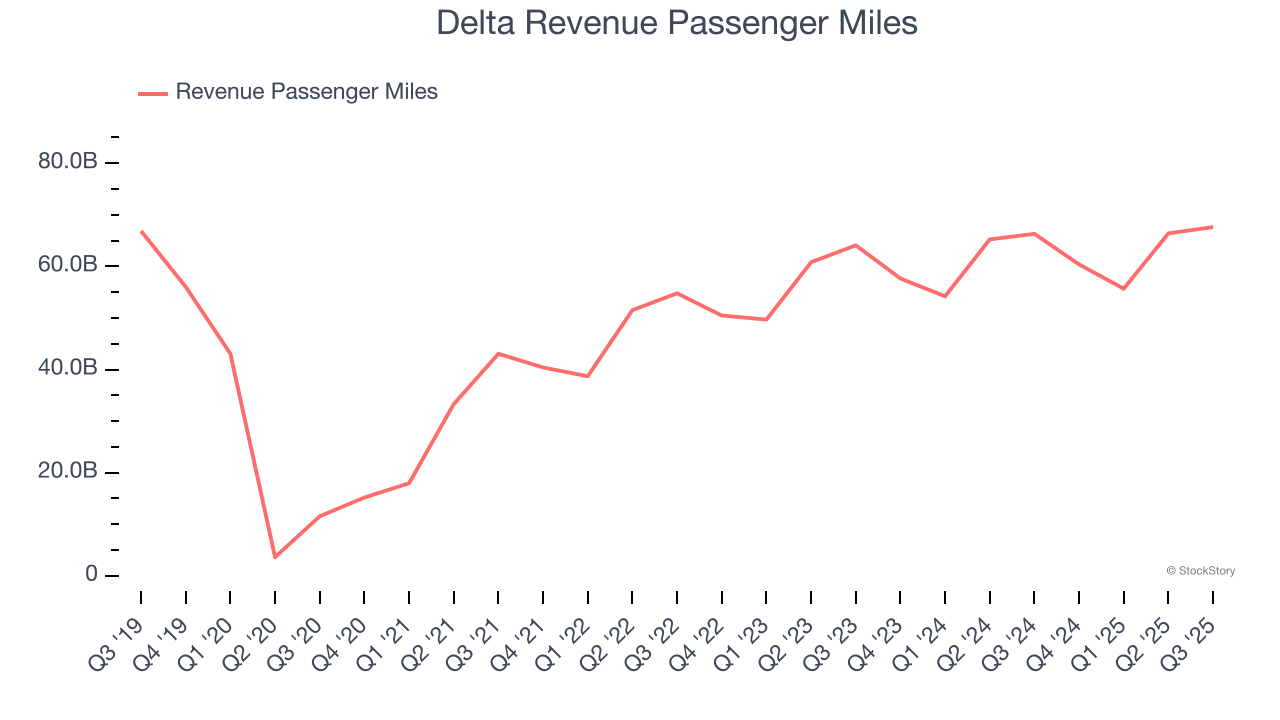

- Revenue Passenger Miles: 67.62 billion, up 1.31 billion year on year

- Market Capitalization: $37.05 billion

"Delta's competitive advantages and differentiation have never been more evident, and thanks to the hard work of our people, we continue to elevate the customer experience and extend our industry leadership. We delivered September quarter results at the top end of our expectations on a combination of strong execution and improving fundamentals," said Ed Bastian, Delta's chief executive officer.

Company Overview

One of the ‘Big Four’ airlines in the US, Delta Air Lines (NYSE:DAL) is a major global air carrier that serves both business and leisure travelers through its domestic and international flights.

Revenue Growth

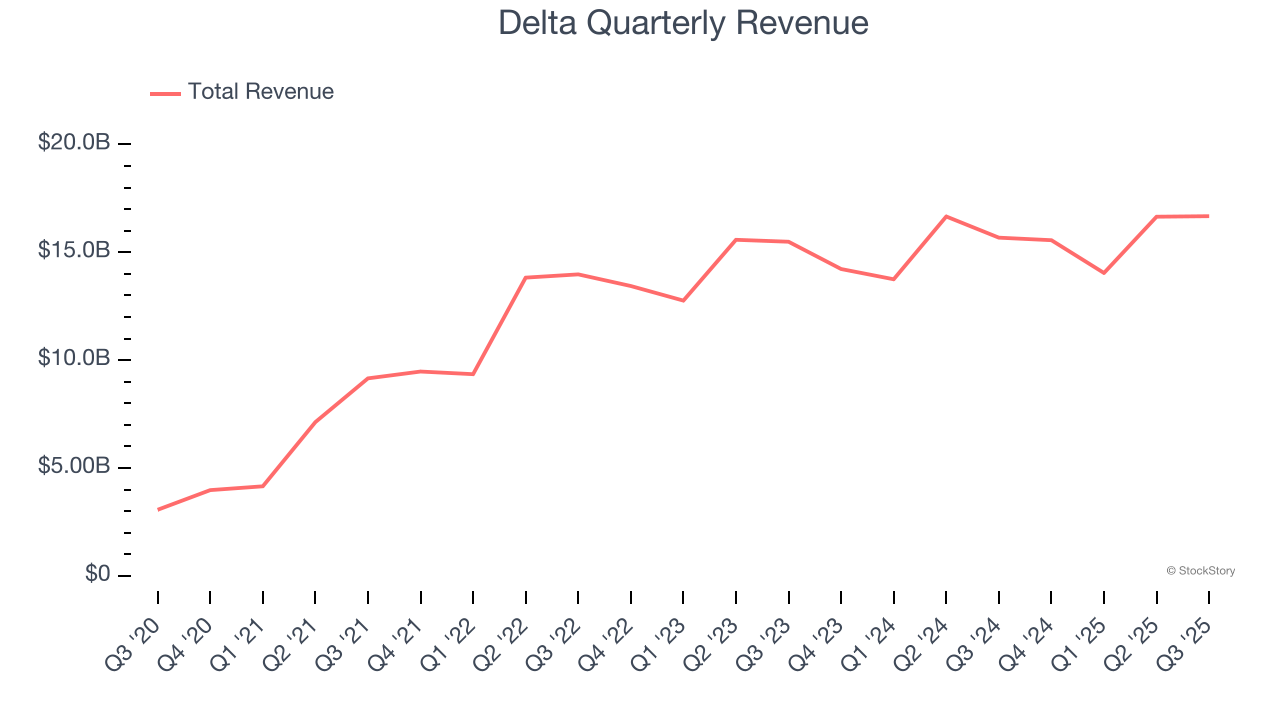

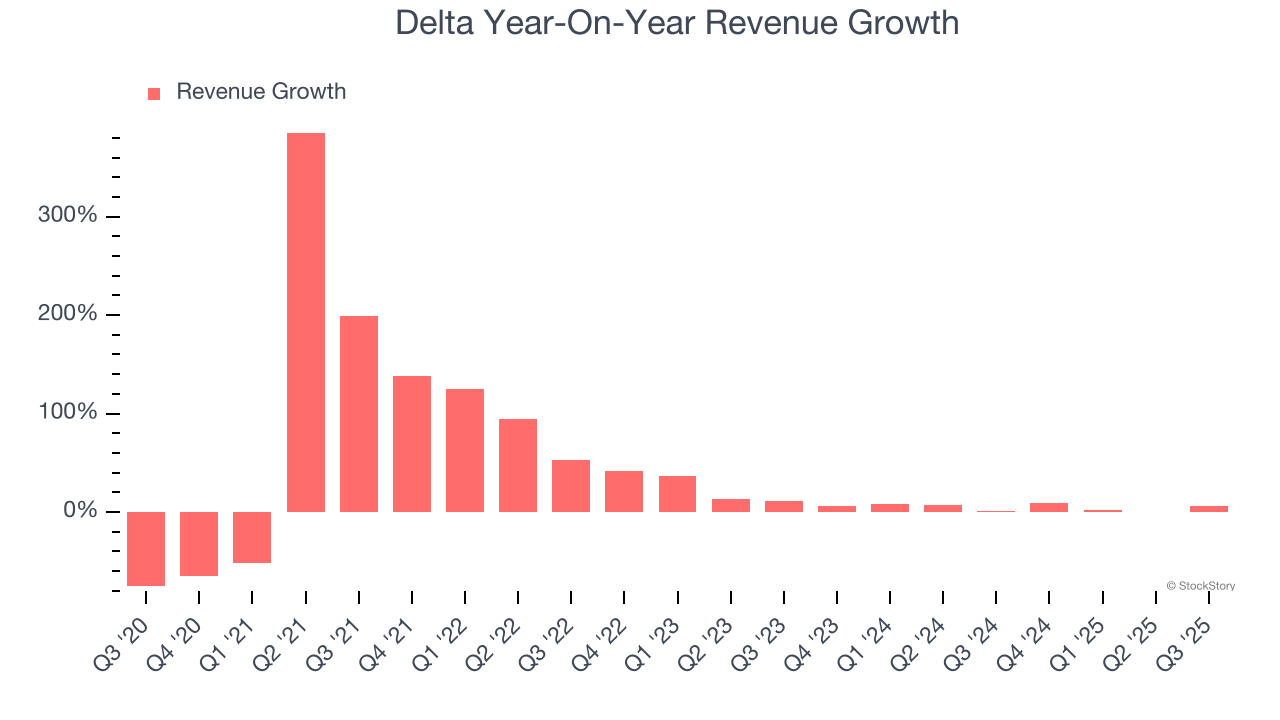

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, Delta’s 20.7% annualized revenue growth over the last five years was solid. Its growth beat the average consumer discretionary company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new property or trend. Delta’s recent performance shows its demand has slowed as its annualized revenue growth of 4.8% over the last two years was below its five-year trend.

Delta also discloses its number of revenue passenger miles, which reached 67.62 billion in the latest quarter. Over the last two years, Delta’s revenue passenger miles averaged 5.7% year-on-year growth. Because this number aligns with its revenue growth during the same period, we can see the company’s monetization was fairly consistent.

This quarter, Delta reported year-on-year revenue growth of 6.4%, and its $16.67 billion of revenue exceeded Wall Street’s estimates by 3.8%. Company management is currently guiding for a 3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 2.7% over the next 12 months, a slight deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will face some demand challenges.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

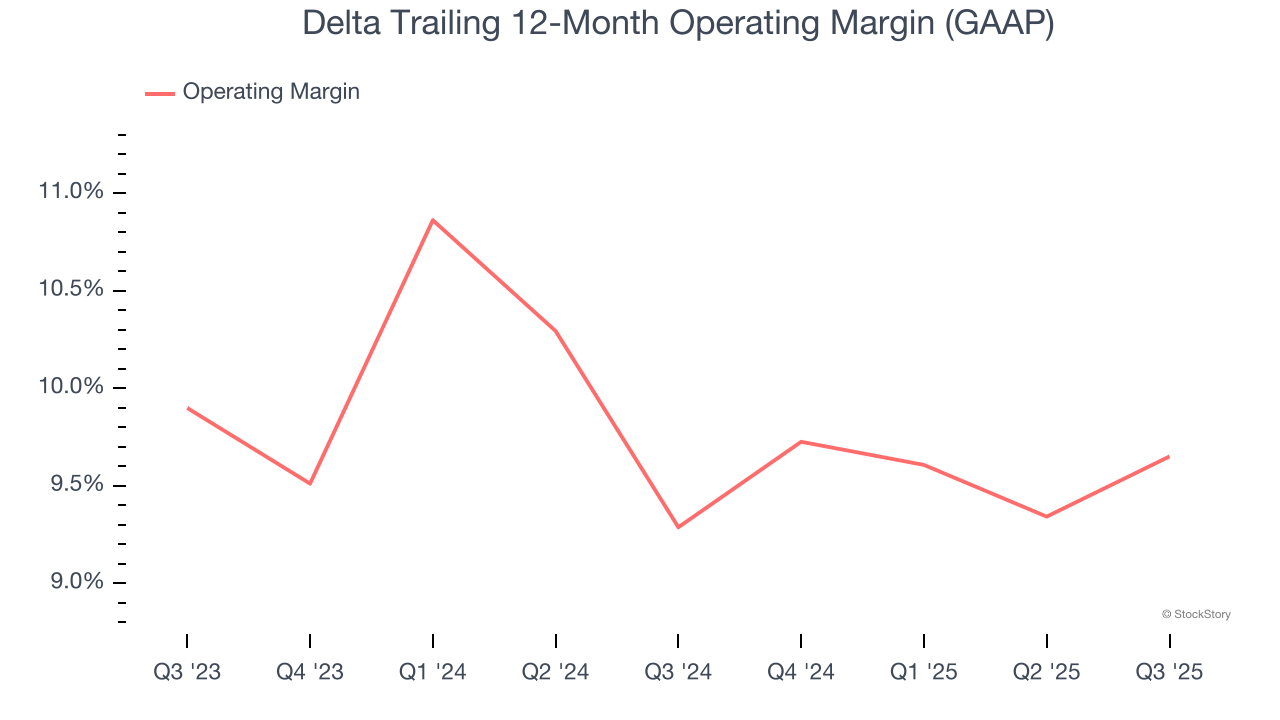

Delta’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 9.5% over the last two years. This profitability was mediocre for a consumer discretionary business and caused by its suboptimal cost structure.

In Q3, Delta generated an operating margin profit margin of 10.1%, up 1.2 percentage points year on year. This increase was a welcome development and shows it was more efficient.

In the coming year, Wall Street expects Delta to maintain its trailing 12-month operating margin of 9.7%.

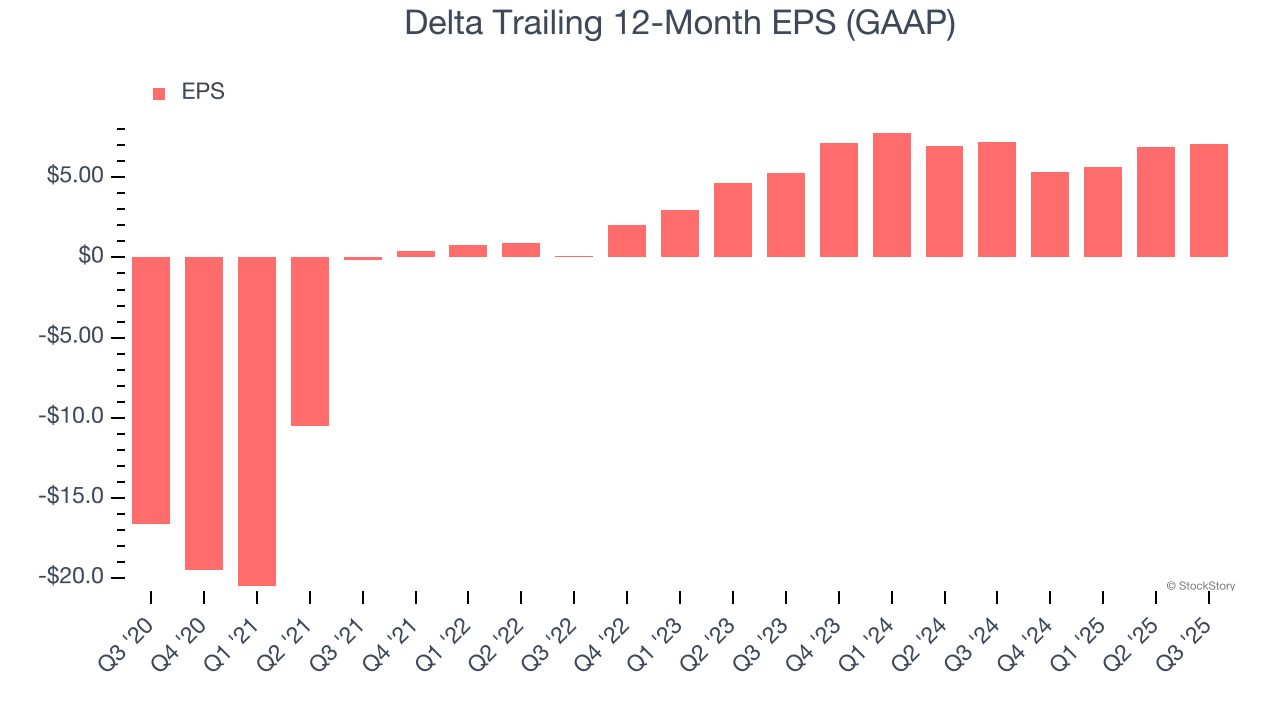

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Delta’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q3, Delta reported EPS of $2.17, up from $1.97 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Delta’s full-year EPS of $7.10 to shrink by 2.5%.

Key Takeaways from Delta’s Q3 Results

We were impressed by Delta’s optimistic EPS guidance for next quarter, which blew past analysts’ expectations. We were also glad its revenue and EPS both outperformed Wall Street’s estimates in the quarter. Overall, this print had some key positives. The stock traded up 7.6% to $61.50 immediately following the results.

Delta may have had a good quarter, but does that mean you should invest right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.