Snap (SNAP) shares pushed meaningfully higher on April 27 after Redburn upgraded the social media technology company to “Buy.”

In their research note, the firm’s analysts doubled their price objective to $10, indicating potential upside of nearly 65% from current levels.

The subsequent surge in SNAP saw it challenge its 100-day moving average (MA) on Monday. A decisive break above $6.20 would signal shifting long-term momentum in favor of the bulls.

Note that Snap stock is currently down about 30% versus its year-to-date high.

Why Did Redburn Turn Bullish on Snap Stock?

Redburn’s optimism is rooted in SNAP’s successful transition away from a pure-play advertising model.

While digital ads remain the core engine, the investment firm recommends loading up on Snap mostly for its commitment to rapidly scale its premium subscription service, Snapchat+.

According to analysts, SNAP’s subscription revenue will more than double to $1.75 billion within the next three years, growing its share in total sales from 13% to a whopping 22%.

This emerging shift, they believe, offers a more predictable, recurring cash flow that insulates the company from the notorious volatility of the digital ad market, potentially driving Snap shares higher over time.

AI and Cost Cuts to Drive SNAP Shares Higher

Another major pillar of Redburn’s bullish call on SNAP stock is management’s focus on sustainable earnings that recently prompted aggressive cost cuts.

The company likely reached a breakeven on a GAAP basis last year (excluding experimental hard-ware ventures like Spectacles), and is strongly positioned to become “meaningfully profitable” in 2026, it told clients.

Beyond job cuts, this is supported by Snap’s pivot toward an artificial intelligence (AI)-enabled operating model.

These efficiencies are designed to push gross margins above 60%, reassuring investors that SNAP is finally maturing into a lean, profit-generating machine, Redburn concluded in its research report.

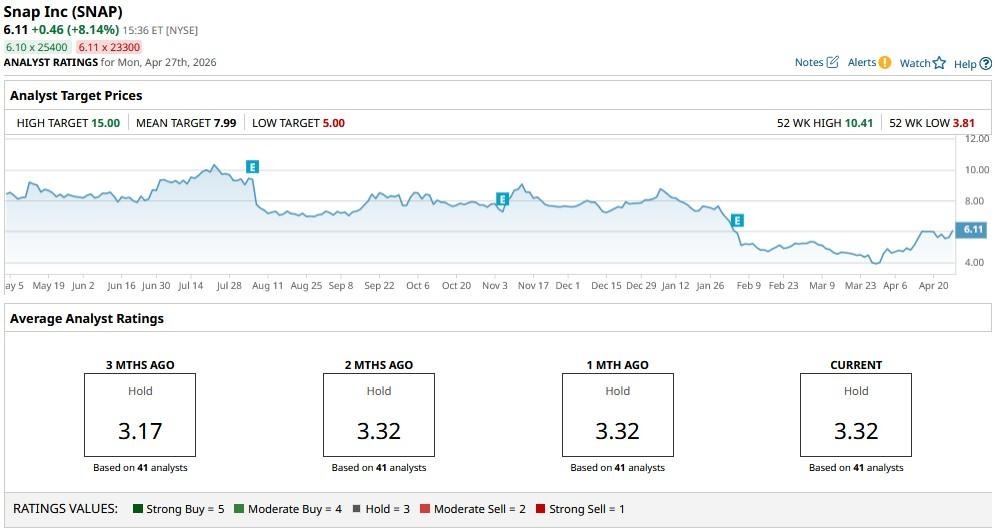

What’s the Consensus Rating on Snap?

While not nearly as bullish as Redburn, other Wall Street analysts haven’t thrown in the towel on SNAP shares either.

The consensus rating on Snap sits at “Hold” currently, but the mean price target of about $7.99 signals potential upside of more than 30% from here.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart